Credit unions must be trusted, not subjected to the dead hand of the State

The new tiered regulations will lead to better-value banking services for all, writes Kevin Johnson

Kevin Johnson

PUBLISHED 03/01/2016

Since its foundation in 1958, the credit union system has flourished in Ireland, both in urban and rural communities. The value that credit unions bring to Ireland is rooted in the simple co-operative business model of people saving together and lending to each other at affordable interest rates.

Despite the lip service paid to the ideal of preserving credit union uniqueness, we fear that uniqueness will be steadily chipped away over time and ultimately lost, unless clear steps are taken and constant vigilance is maintained to ensure that the rules evolve with the diverse needs of ordinary people.

There has to be appropriate rules for each type of financial institution. Similarly, there have to be appropriate rules proportionate to the nature, scale and complexity of each credit union, as recommended by the Commission on Credit Unions.

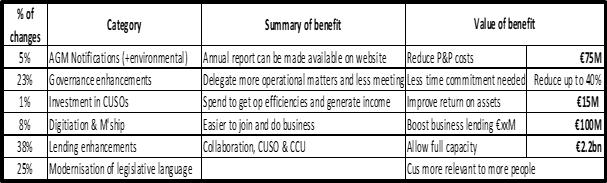

The blueprint for the future of credit unions in Ireland was set out in the Commission’s report, published back in April 2012. This was a comprehensive set of recommendations, including a tiered regulatory framework, which was endorsed by all the stakeholders involved, including credit union representative bodies and the Central Bank.

The Commission’s report provided a factual insight into the financial position of credit unions; it looked at international best practice and presented its views on where the credit union movement in Ireland should be headed.

It went on to make proposals for stabilising and restructuring the sector and for strengthening the legislative and regulatory frameworks, including an improved governance regime. This was adopted as government policy, resulting in the Credit Union Act of 2012.

Our ongoing concern, as expressed by us and other key stakeholders throughout 2015, is that the Central Bank seems determined to implement regulations in a manner inconsistent with the spirit and intent of what was agreed. On top of all the new costly responsibilities that credit unions had to implement, the Central Bank was imposing further restrictions on all credit unions.

These limit how much people can save in their credit union and, critically, the nature and term of lending that credit unions can provide.

Recently, the Minister for Finance commenced the remaining sections of the 2012 Act which activated these regulations.

In doing so, Mr Noonan confirmed that he instructed the Credit Union Advisory Committee (CUAC) to carry out a review of the implementation of the recommendations set out in the report of the Commission on Credit Unions. This will commence immediately and conclude in June 2016.

While it must be recognised that this review should not be necessary, it is clear that it is needed. Unfortunately for consumers, it would have been more practical to see it conducted before the new regulations were effected. However, it presents a chance to get back on track with the blueprint for the future of credit unions in Ireland as originally set out.

The Registrar of Credit Unions has now confirmed that some credit unions will be allowed apply to accept deposits of over €100,000. While this will be welcomed by all large credit unions, and particularly by those credit unions that have built scale following a merger, the real benefits will flow to consumers as this is a first step in the establishment of tiered regulation.

Tiered regulation, done properly, will allow some credit unions to continue to offer basic savings and loans, while allowing other credit unions to develop and offer a greater range of services as long as they have what is necessary to manage the additional inherent risks.

Credit unions need to be allowed to compete with banks. For example, restricting them to solely competing with money lenders is doing consumers a huge disservice.

When it comes to global best practice, the Canadian credit union movement is one of the best, delivering low-cost bank-competing products to millions of members. Their success is based on the fact that they are organisations inspired by the community and working for the community. Their ethos is identical to Irish credit unions, but their regulation, operations and success for consumers are vastly different.

Fundamentally, credit unions offering a full range of account and financial services, from debit card to mortgages to pensions, will drive greater competition, something that is sorely lacking in Ireland at the moment.

We see real potential to replicate much of that model, which could see credit unions across Ireland prudently lend a further €7bn in short, medium and long-term finance.

This is good for consumers on so many levels – apart from ensuring fair interest rates and fees in the market, it allows people to be part of a highly networked community focused on economic, social and environmental change.

For any government – sitting or potential – to be taken seriously in its stated goal of preserving the ethos and philosophy of credit unions, we feel it must demonstrate that regulation is about balance: on the one hand ensuring that consumers have access to basic financial services on competitive terms, while on the other hand, ensuring that the provider does so without taking on too much risk.

Unfortunately, in the last few years, the pendulum had swung too far to over-zealous regulation.

The vast majority of credit unions are financially sound, compliant, competent and ready to provide more services to more people.

The acknowledgment of the role of tiered regulation will enable most, but particularly those with scale and expertise to offer the services that their members rightly expect from a modern credit union.

Kevin Johnson is chief executive officer of the Credit Union Development Association (CUDA)

Sunday Indo Business

http://www.independent.ie/business/irish/credit-unions-must-be-trusted-not-subjected-to-the-dead-hand-of-the-state-34331204.html